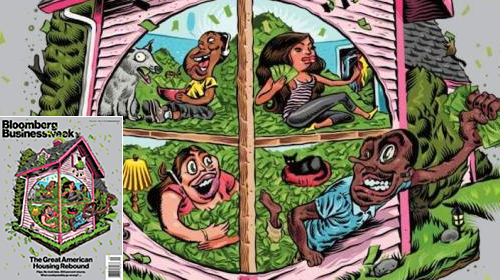

Bloomberg Businessweek’s Racist Cover Dismisses Housing Discrimination Against Communities of Color

To illustrate its cover story about the housing market’s recovery in Phoenix, last week’s Bloomberg Businessweek cover depicted four black and Latino caricatures with obscenely exaggerated features, celebrating in a house filled with cash. You might wonder why an article about a tentative economic upturn should be represented by such alarmingly racist stereotypes—as though it’s a problem that people of color to have access to credit. After intense blowback, Bloomberg Businessweek responded, asserting “Our cover illustration last week got strong reactions, which we regret. Our intention was not to incite or offend. If we had to do it over again we’d do it differently.” However, their “apology” and its focus on their “intention” misses the larger point: Reducing complex economic systems to a caricature, particularly when it is done with an agenda, obscures the real sources of inequality and unfairly blames the victim.

In actuality, a recent Brandeis University report—ironically released the same week as the Bloomberg cover—found the black-white wealth gap tripled between 1984 and 2009. The study found that the single largest contributor to this explosive increase in inequality is that white families have a longer history of homeownership than their black counterparts, in part due to the American legacy of segregation and lending discrimination.

Indeed, even in the 21st century, communities of color have been unfairly targeted by the lending boom and disproportionately affected by the housing bubble crash. They have also disproportionately suffered in the recent recession. Much of such households’ vulnerability has come from unwarranted exposure to predatory subprime loans, which put borrowers at excessive risk of foreclosure.

Minority exposure to the subprime mortgage market ballooned in the years before the 2008 economic downturn, as investment banks like Morgan Stanley and Goldman Sachs pushed subprime lenders to sell thousands of increasingly toxic loans, usually to resell to investors as securities. In historically segregated cities, it was easier for these lenders to pass these loans on minority borrowers—those who had no other choice because better credit had been historically denied. A 2000 joint report from HUD and the U.S. Department of Treasury found that “borrowers in 32 black neighborhoods [were] five times as likely to refinance in the subprime market than borrowers in white neighborhoods,” even when controlling for income. By 2010, African Americans and Latinos were 47 percent and 45 percent more likely than whites to face foreclosure as a result of these loans, respectively.

The effects of this discrimination are still being felt. This is why the ACLU, in partnership with Lief Cabraser, Heimann & Bernstein, LLP and the National Consumer Law Center, filed Adkins et al. v. Morgan Stanley et al., a suit on behalf of African-American homeowners in Detroit who were harmed by Wall Street’s role in fueling abusive lending practices. The case seeks to hold Morgan Stanley accountable for orchestrating the high-volume sale of these crippling loans in Detroit, disproportionately impacting borrowers of color in violation of the federal Fair Housing Act. In a time where the complexities of lending discrimination and wealth inequality are still reduced to racist caricatures, the ACLU is proud to represent plaintiffs with the courage to hold accountable the true culprits—the drivers of toxic lending on Wall Street.

Learn more about housing discrimination and other civil liberty issues: Sign up for breaking news alerts, follow us on Twitter, and like us on Facebook.

Related Issues

Related Content

-

North DakotaJul 2026

Free Speech

LGBTQ Rights

Thunderhawk V. Morton County. Explore Case.Thunderhawk v. Morton County

-

News & CommentaryJul 2026

Racial Justice

+3 Issues

Federal Funding Should Support Communities, Not Political Agendas. Explore News & Commentary.Federal Funding Should Support Communities, Not Political Agendas

Congressional investments should reach the communities they were intended to serve. -

Court CaseJul 2026

LGBTQ Rights

Mirabelli V. Bonta. Explore Case.Mirabelli v. Bonta

In April 2023, a lawsuit was brought challenging a California Department of Education policy preventing public school faculty from outing transgender students without the student’s consent, alleging the law violates the rights of parents. The ACLU opposes the lawsuit in the interest of protecting the privacy and safety of transgender students. -

News & CommentaryJul 2026

LGBTQ Rights

Your Questions Answered: What You Need To Know About The Bpj And Hecox Supreme Court Decision. Explore News & Commentary.Your Questions Answered: What You Need to Know About the BPJ and Hecox Supreme Court Decision

The Supreme Court recently ruled to uphold laws in Idaho and West Virginia banning transgender women and girls from school sports. Learn how the decision impacts transgender people, families, and educators.